The idea of retiring at age 65 with a gold watch and a fully-funded retirement account is a quaint notion for many Americans. Amid stagnating real wages, rising inflation and (still) low interest income, many people have a tough time setting aside money for retirement. And the truth is that there could be multiple problems that Americans face in saving for retirement.

While the 401k is still a suitable available retirement saving option for many people, only 32% of Americans are investing in one, according to the U.S. Census Bureau. That is staggering given that 59% of employed Americans have access to one.

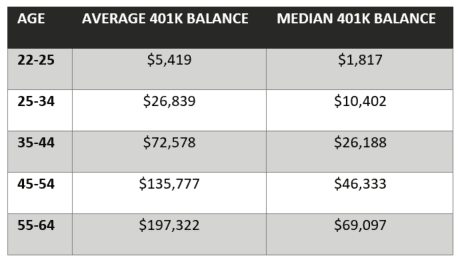

And of the ones who do, an even smaller percentage are saving enough to live well in retirement. Consider these numbers from How America Saves:

So, think these balances are sufficient to support your lifestyle when you retire? Considering that the average life expectancy for women is 86.5 years and for men it is 84 years, possibly not.

You really think that half of those people in the 55-64 age group can live another 20+ years on $3,500 a year?

Sobering Thought #1: Wage Growth

One, the lack of real long-term wage growth in America over the last decade impacts our ability to save for retirement.

It is true that in April 2020 – one of the worst months during the pandemic when the U.S. economy lost 21 million jobs – we saw one of the fastest wage growth periods of all time. You might remember that during that month, the Bureau of Labor Statistics reported that year-over-year growth in average hourly earnings skyrocketed to about 8% -– the highest observed wage growth rate since the series began in 2006.

But that massive increase was because more lower-paid-workers lost their jobs while more higher-paid-workers did not. As such, the “average wage” went up.

Look at it this way: If person A makes $20/hour, person B makes $30/hour and person C makes $40/hour, the “average wage” is $30. But if person A loses their job, then the “average wage” jumps to $35/hour – which is a 16.6% increase.

When changes in data are driven by a shift in underlying characteristics – like more lower-paid-workers losing their jobs – economists call these “composition effects.”

But let’s not get too geeky. Just look at the wage growth over the past 10 years. Prior to last year’s pandemic, wage growth was stagnating.

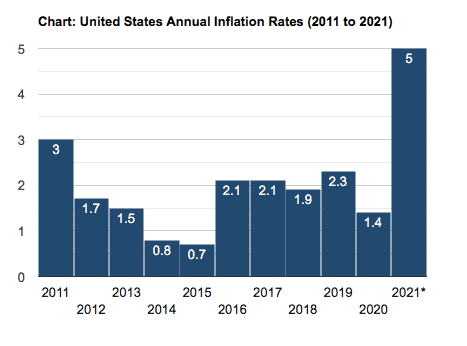

Sobering Thought #2: Inflation

Factor inflation into this equation, and the wage growth story collapses even further. And with less real income, there is potentially less left over to save for the future.

Sobering Thought #3: Low Interest Rates

If low wage growth and rising inflation wasn’t bad enough, think about how the Federal Reserve’s “easy money” policy potentially hurts savers.

Just look at the federal funds rate over the past 70+ years (the fed funds rate is the interest rate at which banks lend to other banks and is set by the Fed). Currently, the fed funds rate is 0.10%.

We used to get a small but significant reward for keeping money in savings accounts, certificates of deposit and government bonds. That’s gone as interest rates are close to zero. Without safe investments like that, many investors may flock into riskier asset classes they know little about.

What You Can Do

You can work towards dynamic financial planning by seeking investment strategies that are custom tailored to your personal aspirations. And while your financial plan may be tied to your long–term goals, short–term events can be addressed too.

Your financial professional can help you manage emotions during investing decisions, help you account for inflation, and work towards an asset allocation aiming for income, growth or both. More importantly, your financial professional can help you balance long–term strategies and short–term tactics in order to help you account for both.

Have specific questions? Don't hesitate to reach out to me today

Wes Garner, CRPC

Principal Wealth Strategist

(281) 269-8669

wgarner@tdecu.org

Important Disclosures

All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments.

Asset allocation does not ensure a profit or protect against a loss.

This article was prepared by FMeX.

LPL Tracking #1-05163219